For most of venture history, a billion-dollar valuation was the reward for years of scaling an organization. You raised, you hired, you grew, you crossed the line, somewhere between 300 and 800 people, somewhere between year six and year ten.

Then 2022 Happened

A new species of company appeared. Young enough to still be in the seed-stage on paper. Tiny enough to fit around a small office. Already worth a fortune. I’ve been tracking the pattern for two years, and I think it deserves its own name.

I’m calling them “micro-unicorns”.

What is a Micro-Unicorn?

A micro-unicorn is a company that reaches a $1B+ valuation with fewer than 100 employees, within two years of founding. With all three conditions measured at the moment it became a unicorn.

The definition matters more than it looks. Three dimensions collapse at once: it is young, it is tiny, and it is already worth a fortune. Lose any one of them and you don’t have a micro-unicorn, you have a fast unicorn, or a small unicorn, or a unicorn.

The “at the moment of crossing” rule does real work. A company that hit $1B with 200 people and later cut down to 70 is not a micro-unicorn, it just became smaller with time. We measure at the snapshot when the line was crossed, because that snapshot is the actual physical evidence that something changed in the math of building a company.

In our dataset, out of 961 unicorns analyzed, 32 companies meet the full definition. 26 of those were founded in the AI era (2022+). That cohort of 26 is the population this essay is about.

How We Counted

This isn’t vibes. It’s a systematic study of every venture-backed company that has reached $1B since January 2010.

- PitchBook – full pull of 961 unicorn companies, with valuations, employee histories, capital raised, and investor rolls.

- Dealigence – round-level deal data and headcount tracking.

- Primary research – direct verification of edge cases and recent rounds.

Timeframe: January 2010 through June 2026, which is basically when the world began to spin for this capital era.

Sources are linked at the bottom of this piece. If you want to dig into the underlying data, ping me.

The Honorary Class

A handful of pioneers took slightly longer than two years to cross $1B but did so lean, and they led the way. They don’t fit the strict definition. They get named anyway, because they’re the proof points the rest of the cohort is built on: Cursor, Magic.dev, Zyphra, and even the Israeli DoubleAI (AAI).

You can argue about the 24-month cutoff. You can’t argue that these four didn’t change what the industry thought possible.

★ The Leaderboard

Seven flagship micro-unicorns, ordered by team size at $1B.

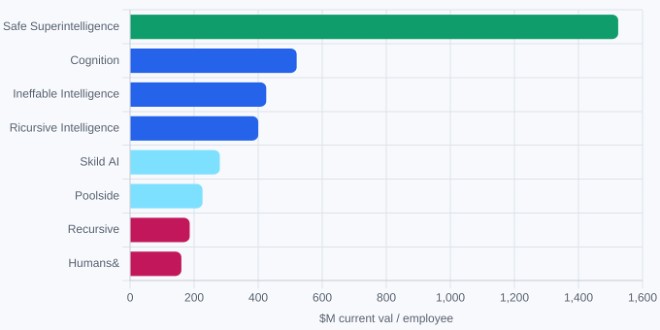

- Inflection AI – 7 employees at $1B · $176M value/employee when becoming a micro-unicorn · $4B current valuation

- Safe Superintelligence (“SSI”) – 10 employees at $1B · $500M value/employee when becoming a micro-unicorn · $32B current valuation

- Cursor (honorary) – 29 employees at $1B · $86M value/employee when becoming a micro-unicorn · $60B current valuation

- Skild AI – 44 employees at $1B · $34M value/employee when becoming a micro-unicorn· $14B current valuation

- Physical Intelligence — 46 employees at $1B · $52M value/employee when becoming a micro-unicorn· $11B current valuation

- Cognition — 50 employees at $1B · $40M value/employee when becoming a micro-unicorn· $26B current valuation

- Poolside – 62 employees at $1B · $48M value/employee when becoming a micro-unicorn · $14B current valuation

Five years ago, these figures were a typo. Today it’s reality.

What the Data Shows

1. The AI Era is Different. By a lot

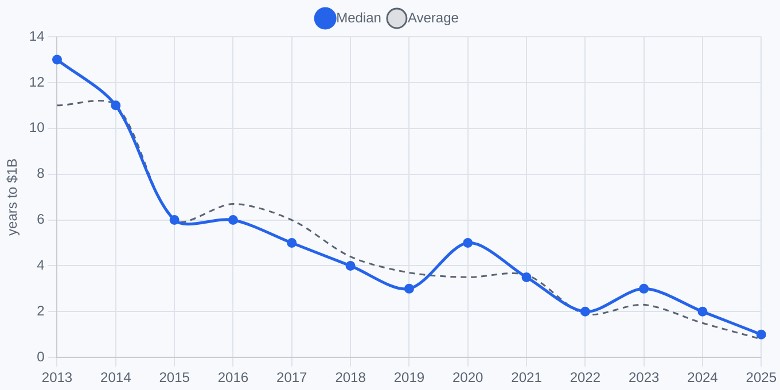

Time-to-unicorn has fallen from roughly a decade (2013 cohort) to under one year (2025). Team size at crossing has trended down to a median of 27 employees for the 2025 cohort.

- 81% of all micro-unicorns were founded in the AI era (2022 or after). And actively looking for one in Israel is a challenge that I accept.

- 50% of them were founded in 2025 alone – 13 companies in one year, more than the entire 2010–2021 period combined.

- AI-era average time to $1B is 1.7 years. For every other company founded between 2010–2021, it was 5.1 years.

The micro-unicorn barely existed before 2022. Now it’s emerging.

2. Time is Shrinking. So Are the Teams

Time-to-unicorn has collapsed from roughly a decade for the 2013 cohort to under a year for 2025. Median team size at crossing for the 2025 cohort: 27 employees.

This is not a marginal compression. This is a category change.

3. Segmentation: What These Companies Actually Do

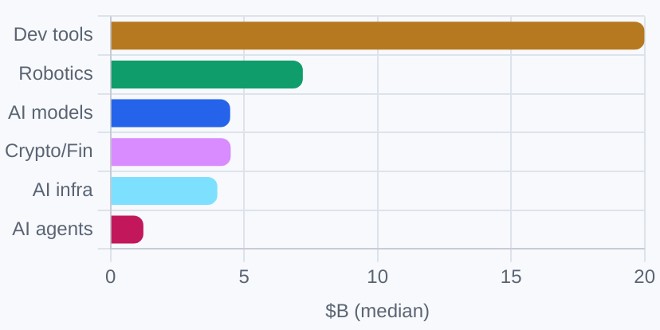

69% of the micro-unicorns are pure AI plays, led by scientists. Here is the breakdown:

- Frontier model labs – 42% share · $4.5B median valuation

- Robotics – 15% share · $7.2B median valuation

- AI infrastructure & chips – 12% share

- Dev tools – 8% share · $20B median valuation

- AI agents – 8% share

- Others – 12% share

Robotics is the strongest broad segment. Dev tools show the highest median but on a tiny sample, be careful with that number. For models, the $4.5B median is the honest figure; the average is inflated by SSI at $32B.

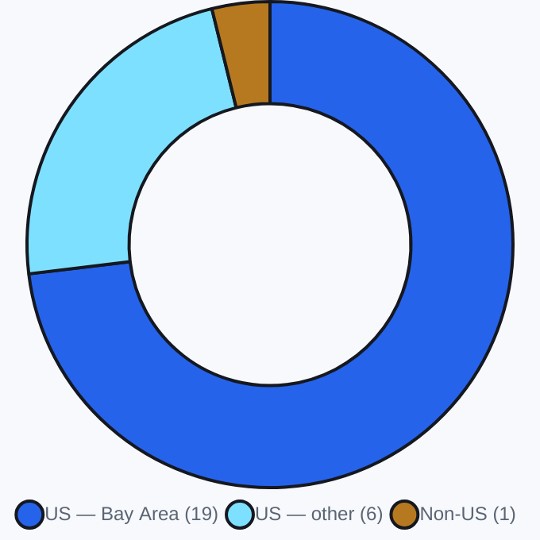

4. Geography: Almost a One-City Story

Of 26 micro-unicorns: 25 are US-based and 19 of them are in the San Francisco Bay Area (and one from the UK). That concentration is the single biggest opening for every ecosystem that isn’t the Bay Area. We’ll come back to this.

5. Micro-Unicorns vs. All 961 Unicorns: The Core of the Thesis

These are the metrics that matter. Everything else is supporting evidence.

- Median employees — All 961 unicorns: 400 · 26 micro-unicorns: 34 · ~12× leaner

- Median valuation — All 961 unicorns: $1.97B · 26 micro-unicorns: $4.00B · 2× higher

- Median value / employee — All 961 unicorns: $5.5M · 26 micro-unicorns: $118M · ~21×

The median unicorn generates $5.5M of value per employee. The median micro-unicorn generates $118M. That is more than 20x the leverage.

6. Exits: The Leverage Shows Up at the Finish Line Too

Five recent acquisitions of micro-unicorn-shaped companies:

- Cursor – acquired by SpaceX · Jun 2026 · $60B exit · 700 employees · $86M/employee

- xAI – acquired by SpaceX · Feb 2026 · $250B exit · 4,900 employees · $51M/employee

- io Products – acquired by OpenAI · May 2025 · $6.5B exit · 55 employees · $118M/employee

- GenMat – acquired by Comstock · Oct 2024 · $2.76B exit · 12 employees · $230M/employee

- Tabular – acquired by Databricks · Jun 2024 · $1.0B exit · 39 employees · $26M/employee

Median exit value per employee is ~$86M. Orders of magnitude above conventional M&A.

What is the buyer actually buying? In frontier AI, an acquisition at this stage is rarely about revenue or the product. It’s a pure talent and market share play. The price reflects the scarcity of the scientists and the value of denying them to rivals. That is precisely why a pre-revenue 12-person company can command billions. io Products (acquired by OpenAI) and the SpaceX–xAI consolidation are pure talent acquihires.

7. Employee Efficiency

- $80M – median valuation per current employee.

- $118M – median valuation per employee at the $1B moment.

- 15–21× – leverage vs. the 961-unicorn population’s $5.5M baseline.

A note on revenue-per-employee: PitchBook discloses revenue for almost none of this cohort, because most are pre-revenue frontier labs priced on capability.

8. Who Backs the Micro-Unicorns: The Single Most Striking Number

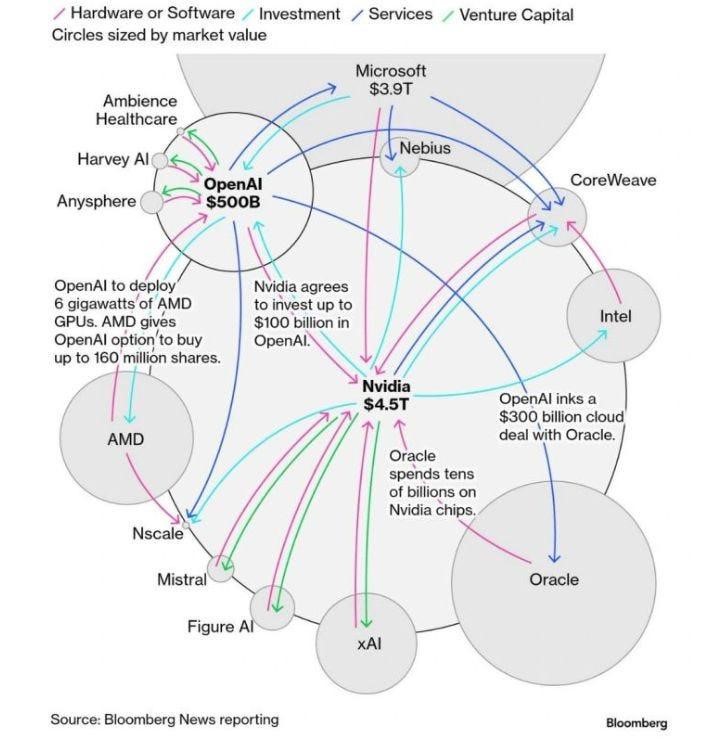

Across the 26 companies, there are 455 unique investors. The cohort is top-heavy with 9 VCs and 3 individuals across all micro-unicorns. And the most prolific backer is not a venture firm: Nvidia is invested in 11 of the 26 micro-unicorns. The computer supplier whose chips these companies run on is also their most prolific investor, financing the ecosystem that drives its own demand. We’ll come back to what that means in the risks section.

Counterpoint · Threats & Risks

The bullish case is strong. A credible internal view has to hold both sides. Three structural risks could blunt the thesis and each follows directly from the very traits that make these companies remarkable.

- Underwriting Capability, Not Execution – Venture capitalists value what a company could become. Customers value what it is today. The micro-unicorn’s valuation is built on the former, a tiny team’s potential. But durable revenue depends on the latter. What enterprise customers want is an enterprise-grade vendor: reliability, security, SLAs, account management, roadmaps that survive a key departure, and the middle-management layer that an enterprise relationship actually runs on: people to own accounts, manage delivery, handle escalations, and translate a research team’s output into a supported product. These are the two things a 20-person company definitionally lacks.

- Talent Density Is Also Talent Concentration – The micro-unicorn runs on a thin layer of exceptional people, and that same layer circulates through the same companies in the same place. Founders and early teams come overwhelmingly from a handful of labs (OpenAI, DeepMind, Anthropic, Meta FAIR) and a single metro (the Bay Area). When value is concentrated in so few people, the firm is acutely exposed to talent migration. A departing founder or poached research lead can move a meaningful fraction of the company’s worth to a competitor overnight. We have already seen it, Inflection’s team to Microsoft, Adept’s founders to Amazon. Leverage per employee cuts both ways. The higher it is, the more fragile the company is to losing any one person.

- The Closed-Loop Market – This is the one nobody likes to say out loud. Nvidia is the most prominent investor in this cohort (11 of 26) and the dominant supplier of the compute every one of these companies depends on. Capital flows from Nvidia into the micro-unicorns. Much of it flows back as GPU spend. That is a closed loop. It can inflate demand in a self-reinforcing circle. It echoes vendor-financing dynamics that have preceded past tech corrections. If frontier-compute economics shift, a cohort financed inside that loop is exposed in a way diversified, customer-revenue-funded companies are not.

Bloomberg Oct 2025 — the AI money loop

The Israeli Opportunity

The geography paragraph is the one I keep coming back to. That is not a verdict on the rest of the world. That is an unclaimed territory. And the traits the micro-unicorn rewards map unusually well onto Israel’s structural strengths.

Why Israel Is Structurally Positioned

- The Micro-Unicorn Rewards Talent Density Over Headcount. Israel’s defining export is high-density technical talent trained under constraints, not from one unit, but from a whole pipeline: Unit 8200, Mamram, Talpiot, Unit 81 and Unit 9900, the Air Force and Naval tech corps. These units train engineers to ship production systems in tiny teams, years before peers finish university.

- The Capital Is Already Pointed at the Right Segments. In 2025, 70% of Israeli tech capital went into cyber and AI, exactly where micro-unicorns form.

- The Ecosystem Has Proven Extraordinary Resilience. Across 2024–2025, through war and mobilization, Israeli tech delivered a record ~$80B in exits in 2025, fundraising near the 2021 peak, and rising founder optimism.

- The Moat Thesis Fits the Israeli Playbook. “If your moat is code, you have no moat.” That points the advantage toward proprietary data, deep workflow integration, infra and cyber — historically Israel’s strongest categories.

”The one-person unicorn is still half a joke. But the sub-100-employee unicorn is already here, and in five years it will be the default, not the exception.” – me, on stage, last month.

The Gap Israel Needs to Fill

Israel is producing AI-era unicorns at remarkable speed and none of them are micro-unicorns (except some unofficial announcements and rumors). Every recent Israeli unicorn founded 2022 or later crossed $1B only after scaling past 100 employees or took longer than two years. The fastest pattern we see is a company that sits in the 30 to 60 employee range for most of its life and then jumps past 100 in the months before the $1B round closes. One name came within sixty days of being a micro-unicorn and crossed at 120 instead. Israel has the speed. Israel has the AI focus. Israel should become the new micro-unicorn producer.

That gap is the opportunity. We name it, then we own it.

What Israel Needs To Do Next

The Bay Area’s micro-unicorns are not magic. They’re a repeatable formula: a tiny team of world-class AI scientists, frontier compute, and capital priced on capability. Israel can run that formula — but only if it builds the one input it is shorter on: depth in frontier AI research talent.

- Grow AI Scientists in the Academy. Expand graduate-level AI/ML research capacity, retain researchers who leave for US labs, and tighten the academia-to-startup pipeline so a PhD’s research becomes a company, fast.

- Grow AI Practitioners Inside the IDF. The elite units (8200, Mamram, 81) already produce the world’s best applied engineers. Make them frontier AI-native – training to build and fine-tune models, run large-scale training, and ship AI research, so alumni leave as model builders, not as engineers. This is the highest-leverage move: it scales the exact talent the micro-unicorn needs, through an institution Israel already excels at.

- Import the Playbook Explicitly. Price first rounds for capability the way US investors do. Build or attract frontier-compute access domestically — and the strategic-compute capital that is currently absent from Israeli rounds. Back tiny, scientist-led teams at seed rather than waiting for headcount and traction.

What’s Next?

This is the part where Medium essays usually wind down to a polite “thanks for reading.” Not this one.

I want to invest in one of the first Israeli micro-unicorns.

A team under 100. Founded 2024 or later. Built around a small group of frontier-AI talent, researchers and not only engineers. The kind of company that would look right at home in the Bay Area, except it’s coming out of Tel Aviv, Haifa, or Be’er Sheva.

If you are building this, or know the people who are, reach out.