VC 3.0: The Next Generation of Venture Capital

Venture Capital always seemed to be the most stable/never changing business — yes, GPs change and investment trends shift, but the business and its operational concepts seemed to remain stable for a long while. It seems that the founding fathers of the industry were thinking mostly like public investors — most of the effort was poured into finding the right investment. From there, the thinking was good investors do not need to be very involved since good startups do not need much help.

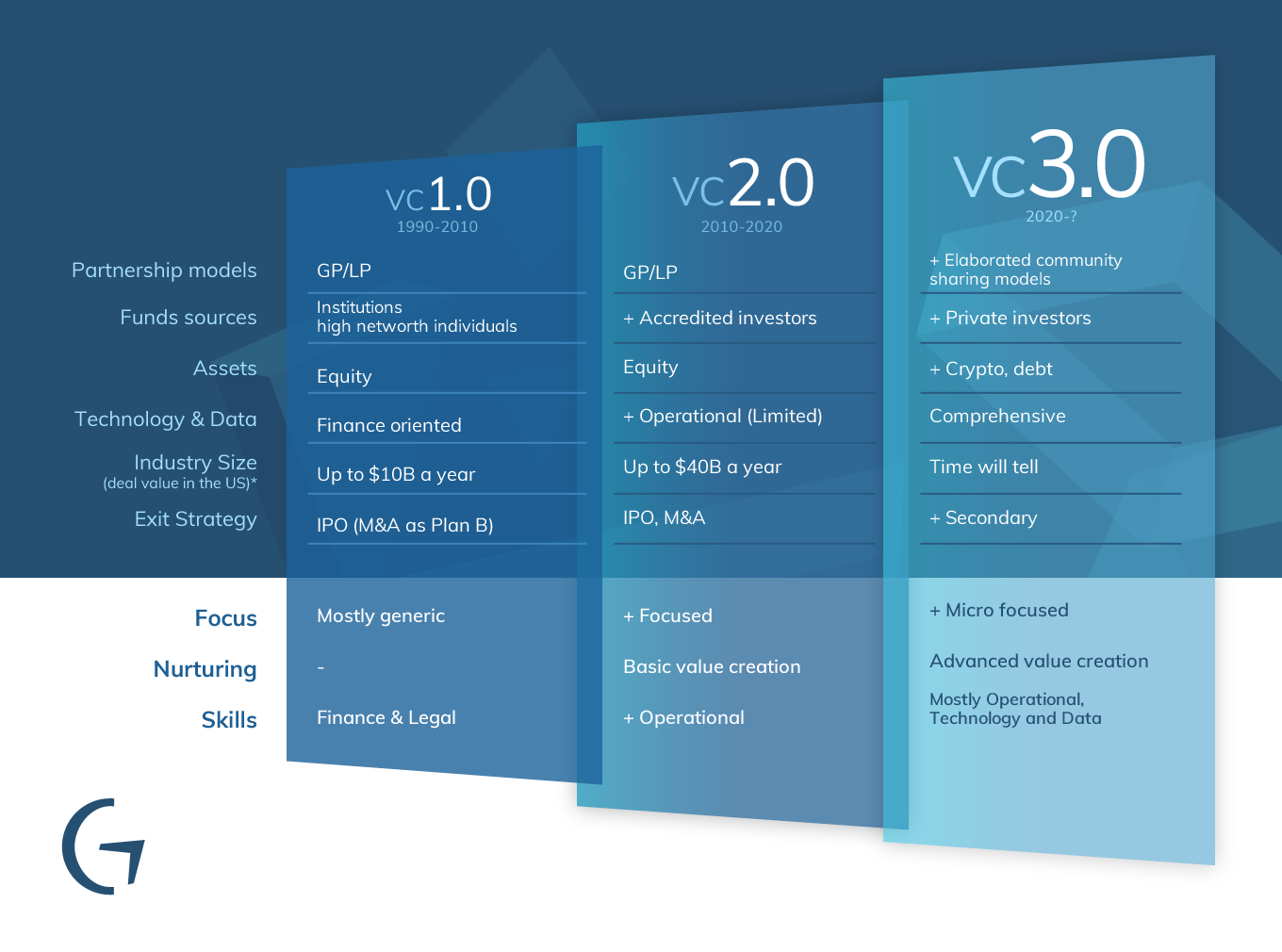

This line of thinking was driven mostly by public investment and day-to-day reality did not change for a while. Most Venture Capital firms have been very similar with regards to most of their business aspects: a partnership model, fund sources, assets, skills, the use of technology and data, and the level of nurturing and exiting portfolio companies. The only real difference between VCs was their investment focus, which differed by stage (early-stage investing, late-stage, etc.), markets (i.e. internet, healthcare etc.) or geographies. Still, most VCs were very similar. This led to a mostly rigid venture structure — almost no operational support, relatively big investment teams and very small, if any, operational teams.

Most of the ongoing efforts taken by VCs following an investment were focused on ‘big’ events such as fundraising or an “exit.” Such efforts have been mostly focused on making sure that the investors’ interests are maintained. This led to VC teams that did not necessarily have operational capabilities and even when they did, they did not necessarily have a clear strategy on how (and when) to leverage them.

VC 2.0

Yet, about a decade ago, something changed. Not to say that all VCs changed at once, but as the needs of startups changed, a different type of VCs emerged. It didn’t mean that the era of the Passive VC (let’s call it VC 1.0) was about to end, but rather the addition of a more active model emerged. A group of new VCs started to explore different models, including Andreessen Horowitz (a16z), Y Combinator, 500 Startups and others. For example, Andreessen Horowitz was founded in 2009 by Marc Andreessen and Ben Horowitz, two well-known entrepreneurs with very strong operational backgrounds (Marc was the founder of Netscape and Loudcloud). Not surprisingly, Marc and Ben presented a very different model, based on massive operational power, designed to help entrepreneurs in more than one way. Humbly, in 2010 we at Glilot created our own version of VC 2.0, starting our first fund that was laser-focused (cyber/enterprise SW) and provided strong operational support for portfolio companies driven by our strong thematic focus. Our Value Creation team is focused on helping young portfolio companies find U.S. and European customers, which helps them mature very quickly.

Arik Kleinstien, my co-founder, and I, both have strong operational backgrounds coming from our own ventures, much like the newer VCs, which were often founded by entrepreneurs-turned-investors. These VCs have a better understanding of the everyday operations of young companies, especially after creating successful startups of their own. They were primed to cultivate the next generation of entrepreneurs and willing to offer their experience on top of funding. Erik P.M. Vermeulen and Joseph A. McCahery elaborate on this “new breed of investors” in their book: ‘ Venture Capital 2.0: From Venturing to Partnering’.

To be clear; I am not claiming that there is one typecast of a successful investor/VC. Many successful investors did not necessarily come from operating backgrounds.

Overall, the VC 2.0 period was characterized by several differentiating factors. Firstly, there was more polarization in the industry. Larger firms, such as a16Z, Sequoia and Kleiner Perkins, widened their investment focus, while smaller firms focused on frontier technologies. This created a situation in which mid-sized VCs gradually disappeared. Some VCs became very successful and grew to become big funds, while others found it difficult to compete financially with the larger firms, and couldn’t offer the attention given to companies by smaller funds. Alongside a greater number of startups reaching unicorn status, and large corporations such as Google and Intel creating and cultivating investment arms of their own, the VC space was completely transformed.

Adapt or be left behind

We live in an ultra-agile era. Markets, technologies, and even people change at an ever-rapid pace. This used to be a phenomenon relevant only for companies operating in the rough edges of technology. Not anymore. Every company in virtually any space is required to be agile to sustain itself — from finance, to automotive, to healthcare and retail, advancement and change are eating up the slow-moving beasts and opening great opportunities for the agile, fast-changing animals.

VCs are not different. Yes, we would like to believe that other rules control our lives, but unfortunately, this is not the case. Massive changes are happening around us, forcing us to re-examine our models and adapt to change. In my mind, this is in no way a ‘nice to have’ characteristic. This is a matter of life and death (business-wise of course). Some of the changes to note are:

- The large increase in private financing, including private unicorns, as well as the increased sophistication created in private markets.

- Globalization- The world continues to become more global. Silicon Valley is still the Mecca of venture investing, and yet, other geographies, such as China, Europe and Israel, cannot be ignored anymore.

- Increased competition on the venture capital front, including competition from other, innovative investment platforms such as crowdfunding.

- The relative longer time required to hold a private investment as well as the higher sums required to be raised.

- Cryptocurrencies, as well as underlying technologies such as blockchain, continue to reshape the finance arena.

- Polarization in the VC space. Smaller, niche VCs are taking over “frontier technologies” and areas that require a high level of expertise, while larger VCs are diversifying and investing in companies with a clearer go-to-market strategy.

- Huge increase in corporate investment activity, as more and more enterprises realize how disruptive tech can be to their business.

The 3rd Generation

In April 2019, Andreessen Horowitz announced that it is applying to become a Registered Investment Advisor (RIA). What does a VC have to do with financial advising? Most analysts believe that Andreessen Horowitz desire for more flexibility, which is an essential part of the move. By becoming an RIA, they will be able to do more with their funds, especially since it will no longer be limited to receiving equity. This opens up the door to many possibilities, such as investing in blockchain startups that can offer crypto in return.

This move is the best indication so far for VC3.0. This makes a lot of sense, so much had changed since the firm started its operation, how can anyone suggest that the same strategy is still valid? That it’s still the one most suited for today, and, more importantly, tomorrow? The same goes for us, even though we built our model only 9 years ago, and it is still considered innovative, we are spending a significant part of our time to examine it, reshape it and create a new model that will hopefully support us in the next 4 years or so (Unfortunately, time frames are getting shorter and I am afraid I cannot imagine our new strategy to last for 8 years or more this time).

Reshaping the VC space

So, what are these new strategies all about? Hard to say. Specifically, because my personal bet is that there will be many different ones, suiting specific GPs, specific venture DNA and specific desired outcomes. However, I can draw some lines into the shapes and building blocks of such strategies. To continue this analysis, I will categorize VC by the following criteria:

- Investing

- Nurturing

- Exiting

- Source of funds

- Use of technologies and data

- Compensation model

1. Investing: VC 2.0 brought to life the concept of “expert” VCs: VCs that invest in a specific, possibly narrow, field (such as cyber, or automotive IT). I believe this will continue in VC 3.0. But the focus is not enough, as the Andreessen Horowitz move indicates, I believe we will see funds investing in other types of equity and possibly in other assets classes, such as Bitcoin and other cryptocurrencies, and more. We will also see a mix between different classes — VC/PE/Crypto/Debt etc.

2. Nurturing: VC 2.0 placed an emphasis on Value Creation. Glilot’s strong Value Creation team helps young companies generate sales, and provides support in other areas of startup operations: marketing, talent recruitment, fundraising and more. I believe that this will continue with more force. VCs will create larger, more detailed and sophisticated models of value creation, supporting their portfolio companies in an ever-growing spectrum of issues. From HR to financing, product and sales. Value creation is a great way to attract the best entrepreneurs as well as to add value to LPs.

3. Exiting: In VC 2.0, M&A became a more common method of exiting, creating a complex hybrid model, which deviated from the old and simple model of an IPO. I believe that future VC3.0 will bring an even more complex model. In the past, the secondary sale of shares was almost considered a “bad word” amongst venture capital firms. I believe this will change with a richer secondary market that will provide more opportunities for liquidation, to support longer investment periods and bigger investment rounds, among other reasons.

4. Source of funds: In the classic venture capital model, funding came mostly from big institutional investors or high worth individuals. VC 2.0 brought in more private money, mostly coming from accredited investors, and more specifically crowdfunding. I believe that VC 3.0 will allow the industry to access the individual investor, as well as to create advance models related to funds’ sources.

5. Technology and Data: As an industry, we have been pitching the need for advanced technologies, machine learning and big data, but have largely failed to adopt these technologies ourselves. Yes, VC 2.0 partnerships (including us) have been utilizing such technologies, but this was limited to operational/deal-flow aspects, such as CRM and the likes, which did not have a big impact on the core of the business. I believe that VC 3.0 will bring much deeper use of technology and data (as a reference, please see my colleague Nofar Amikam’s thoughts on data-driven venture capital).

6. Compensation models: The classic venture capital compensation model did not change much while the industry moved from VC 1.0 to VC 2.0. However, I believe it will change now. The difference between today’s VC and VCs of the past is simply too great, and even more so with later and future VCs. Some VCs will adopt community-based models, such as our own revenue sharing model — we are sharing our upside with our entrepreneurs to encourage collaboration between founders of our portfolio companies (please read more here). Other VCs, more specifically bigger VCs investing in wider asset classes, will find that the existing compensation models are simply not relevant. I believe we will see different more elaborate compensation models.

Greater opportunities than ever

I cannot say that I know where we are heading. I am sure of one thing though: the VC world is changing. The environment in which us venture capitalists are operating is changing at a very rapid pace. The bad news: those of us that will not adapt, will most likely lose and even disappear. Even the best investors, if unable to adapt, will fail. The good news: market opportunities are more present than ever. The private equity markets, and more specifically the VC market, are rapidly growing. The role of technology and specifically technology created by young companies is bigger than ever before. Those of us that will adapt and will be able to create smart, agile strategies, will see opportunities unlike any they’ve ever seen.

Dorin Baniel

Dorin Baniel

Kobi Samboursky

Kobi Samboursky{kind=link}

{kind=link}

{kind=link}